Deep Into the Negative

Or, I would make a "Stranger Things" reference but season three sucked

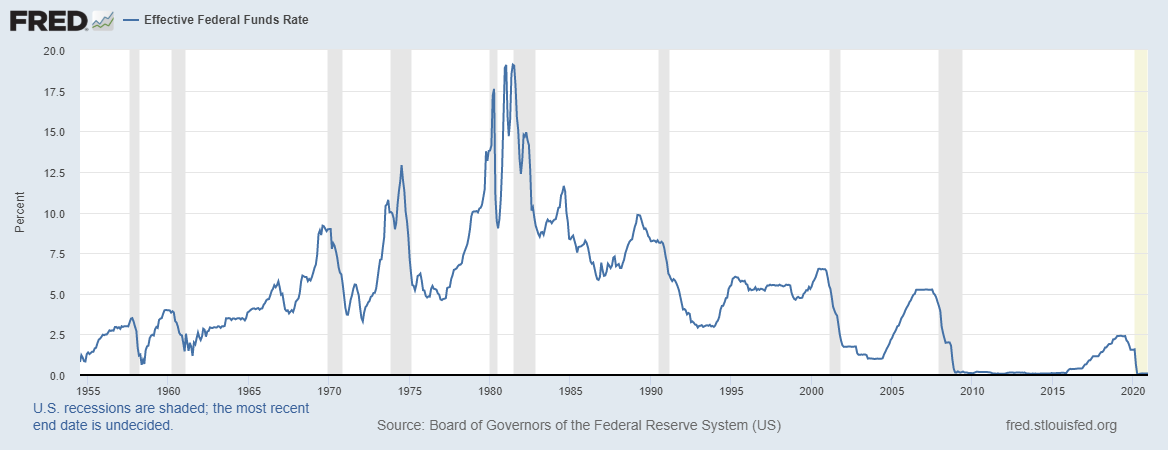

One of the main limitations to effective monetary policy going forward will be that interest rates are at or near zero in much of the world. Without the ability to make large cuts to interest rates, the ability of monetary policy to fight recessions is greatly hindered. Interest rate cuts are, after all, one of the main ways demand is stimulated, by making liquidity and loans easier to acquire.

The good news is that this Zero Lower Bound (or ZLB for short) is a limit by political choice and not economic constraint. In this piece I will discuss why we should break through the ZLB and a way we can break through with little side effects.

Going Negative

A negative interest rate, simply put, means that borrowers earn interest instead of lenders. This has two main effects: 1) borrowing is greatly incentivized, and 2) banks are forced to create more money. It is obvious why the first effect happens. If you can borrow at no cost and even earn interest on what you borrow, why wouldn’t you borrow as much as you can? The second is a bit more obscure because many don’t realize that banks themselves ultimately create money in the modern economy. If more loans are being made, more money is being made, which can boost up inflation and stop a nominal GDP shortfall, which is the ultimate cause of a recession, in its tracks.

The reason why we want the rates to be deep is that deeper rates are more powerful, so they don’t need to be used for a long time. This minimizes the amount of time lenders are getting the short end of the stick and allows the economy to go back to “normal” faster.

We saw during The Great Moderation that interest rate adjustments were very effective in reducing recessions. By allowing interest rates to go deep and negative we can reduce our reliance on quantitative easing and helicopter money to conduct strong monetary policy. Now, I’m not saying I’m not a fan of quantitative easing and helicopter money (in fact I have a piece on the latter planned), but it seems prescient to conduct a minimalist policy most of the time.

Par for the Course

One of the main limitations to achieving deep negative interest rates is that cash, as it stands in our financial system right now, is unaffected by interest rates. If you are an institution losing money on reserves held at the central bank (which is essentially what would happen under a negative interest rate), it would make sense to withdraw large amounts of cash because said cash isn’t affected by the negative interest rate. This, however, would negate the efficacy of the policy.

So it is important to find a way to put the negative interest rate on to cash. What the proposed “Clean Approach” does is create an exchange rate at the central bank’s cash window between cash and “electronic money”, which in this case is the form in which money is held in the bank, in reserves at the central bank, etc. “Electronic money” is the unit of account, or way in which prices are represented, making it “baseline” for measuring our cash against. This exchange rate should mimic other short-term interest rates.

A way exchange rate can be created is via a deposit fee at the cash window of the central bank. If this fee crawls upwards over time it helps to block arbitrage by lifting the exchange rate alongside the growth of interest on electronic money. Essentially, just like how every dollar spent with a credit card would be worth a tiny bit less over time due to the interest rate, each piece of cash would be worth a tiny bit less over time due to the exchange rate created by the timescaled deposit fee.

We know that this cash interest rate would be kept almost uniformly across the financial system. However, it may break down at the retail level, but it already does that somewhat nowadays. Stores actually earn less from credit than from cash, but almost all stores (even when permitted) don’t surcharge cash usage.

As for household transmission, the exchange rate would hold because the electronic money would overwhelmingly be the unit of account for households, thus the adjusted cash worth would be communicated throughout the economic system.

Check Please

I hope this piece has begun to make deep negative interest rates a viable policy tool in your mind. For more information, check out the papers by Miles Kimball and Ruchir Agarwal linked above. This definitely won’t be the last time I write about this topic, too, so stay tuned.

P. S. If you have any suggestions for a topic I should write about, let me know in the comments.

David Beckworth again: “He, Krugman, definitely has a traditional New Keynesian perspective on getting the real interest rate down to its equilibrium or natural rate level, by raising inflation expectations, and thus, doing it appropriately long enough, you’ll get the output gap clear, and you’ll be back to a healthy recovery.”

Complete tripe. R * is a hoax. Investment hurdle rates are idiosyncratic. Business expenditures depend largely on profit-expectations, and favorable profit-expectations depend primarily on cost/price relationship of the recent past and of the present. Cost/price relationships are crucial, and they are particular; they cannot be adequately treated in terms of broad-aggregates or statistical weighted “averages”.

According to Alfred Marshall’s “cash balances” approach, that prescription will backfire. To wit: Alfred Marshall’s cash balances (“Money, Debt and Economic Activity” (2nd ed.; New York: Prentice-Hall 1953), p. 197

“If the public considers its real balances excessive or deficient, forces will be set in motion which will alter the value of the cash holdings of the public, but not necessarily in the fashion desired by the public.

For example, if the public on balance considers the real worth of its cash balances deficient, this will bring about an increase in the demand for money and a decrease in its supply.

The velocity of money will decline, and if prices tend to be sticky, sales, production, implement and payroll will fall off. This will lead to reduced bank lending, a decline in the volume of money, and this will not be compensated by an appropriate decline in prices.

Under these circumstances’ equilibrium is never reached, and the public in seeking to increase its real balances so reduces its effective purchasing power as to create a condition of chronic stagnation.”

Market monetarism is sheer ipsedixism.

10-Year Treasury Inflation-Indexed Security, Constant Maturity (DFII10) | FRED | St. Louis Fed

Adding infinite, artificial, and misdirected money products (LSAPs on sovereigns) while remunerating IBDDs (inducing nonbank disintermediation), generates negative real rates of interest; has a negative economic multiplier; stokes asset bubbles (results in an excess of savings over real investment outlets); exacerbates income inequality, produces social unrest, and depreciates the exchange value of the U.S. $.

(“It is the real interest rate that affects spending”, pg. 19 Marcus Nunes and Benjamin Cole’s “With Market Monetarism – a Roadmap to Economic Prosperity”).

How do you explain real yields continuing to fall at the same time the economy is “slowing”? Link “Fed Leaves Interest Rates Near Zero as Economic Recovery Slows” – NYT

Interest is the price of credit. The price of money is the reciprocal of the price level. An artificial exogenous increase in money products reduces the real rate of interest. An endogenous increase in the utilization / activation of savings products increases the real rate of interest.

Real output is following the distributed lag effect of money flows, volume times transactions’ velocity.