Inflation Isn't Here

A common refrain amongst the economically ignorant nowadays is that “inflation is coming”. They point to massive M2 growth over the past year and the large spending plans of President Biden as reasons for the onset of inflation. In this post I want to produce a whole host of reasons why they have no idea what they’re talking about.

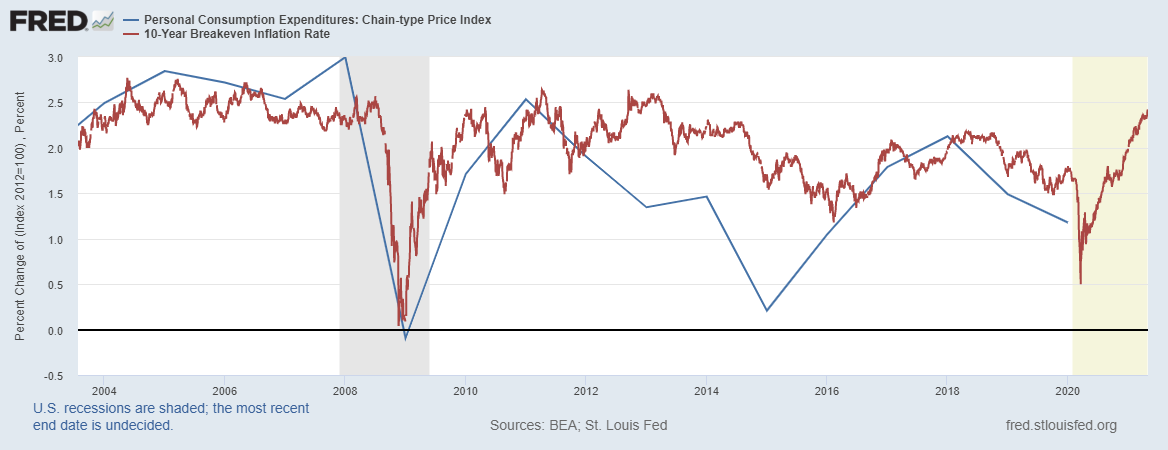

Trust the Market

There has been no better predictor of inflation than the breakeven inflation rate. It successfully called the Great Recession. Let’s see what it has to say:

It’s true that breakevens have climbed steadily higher, but not to any level that may be considered excessive. The last serious inflation was in the 1970s, where we saw between 6-10% yearly PCEPI growth. We are not seeing such. If breakevens do climb that way, we can have another conversation.

The Fed is in Control

I always find any claim of fiscal determination of the price level to be dubious. Thus I don’t find the claim that the large budget deficits favored by Biden will be inflationary to have any merit. Noah Smith argues that there may be 'fiscal dominance'. Again, I am unconvinced. The Fed will not have to raise rates too high to stop inflation, and it has much capacity for forward guidance.

The Fed almost certainly did monetary offset on the stimulus, and I don’t care what Jason Harrison wrote. The Fed determines NGDP. In fact, I’d suggest that the “stimulus” was more deflationary than anything. I don’t see any reason why this isn’t the Fed’s ballgame, which leads me into my next point.

Learn What AIT Means

People seem to be freaking out over these statistics from the BEA. I don’t see why. Even past how misleading YoY is right now, all I see is AIT becoming credible. We lost perhaps a percentage point off of core PCE inflation so the Fed will be doing price level targeting to make up for it. We should not be concerned.

Scott Sumner says that AIT is credible, and I agree. My one concern, which I’ll get into next, is that the Fed is replying on temporary pressures to do makeup.

The Supply Side is (Almost) Everything

The truth is that most of the inflation we are seeing right now is due to temporary supply side measures. The microchip shortage is especially overwhelming, just look at how it affects car prices:

What this means is that 1) inflation will be temporary and affect less, and 2) the way we address it must be different. Microeconomic policy especially has a role here. We must find a way to expand chip supply (hopefully in the context of a R&D bill), expand trade and lower barriers (such as with steel), and wait for market mechanisms. For example, oil, a commodify often assumed to underlie inflation, is quite elastic in supply. It is only with trade barriers that it is not.