Some Common Fallacies in Current Discussions of Market Dynamics

Or, what the hell is going on?

I recently declared that an article in this week’s Economist committed a couple of pretty egregious fallacies of economic reasoning.

I want to use this post to go through this article to deconstruct why I think almost everything it says is tautological or fallacious. This article is a pretty good example of why journalists have few tools to actually understand macroeconomics and should largely refrain from commenting on the subject unless educated better. The opening words of the article outline the two major fallacies it commits:

A “battle of the markups”, between higher wages and higher shop prices, is under way. And there can only be one winner, all else being equal.

First, we have reasoning from a price change, the old enemy of Market Monetarists circa 2011-2014. Next, we have the lump of wealth fallacy, the favorite of anti-immigrant Republicans and internet Marxists since god-knows-when.

Reasoning from a Price Change

Prices, the ultimate signal and one of the most important concepts in economics, change for a multitude of reasons. Much of the work economists do is determining the possible reasons for price changes, predicting what might cause prices to change, and identifying the likely causes of price changes. It is therefore an egregious fallacy to declare that a change in price, or in the price level, is the result of any particular even without good data or a structural model evidencing such.

Yet, this is exactly what this article does. By declaring that the rising price and wage level is the result of a markup battle, the article ignores the far-more-proximate causes of supply chain shortages and higher nominal spending as the drivers behind price markups and wage growth.

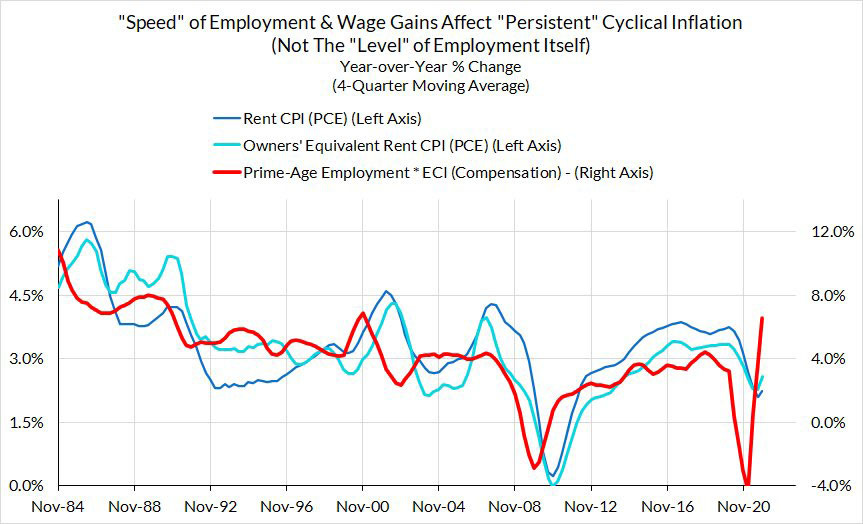

The above chart shows how increases in spending (both in terms of nominal income growth and real growth) lead to both wage growth and price inflation, both as a result of typical nominal dynamics, like expectations adjustment, and labour’s spending putting pressure on prices. However, this implies a future adjustment to a new, higher level of real output, and not a permanent wage-price spiral like the article implies:

…sits America. Here wage growth is rapid, at about 5% a year. But as shown in their most recent financial results, big listed American companies are doing a better job of protecting margins than analysts had expected. A series of unusually large stimulus payments may mean that households are able to absorb the higher prices that companies impose.

The article sets up a correct point here and then… drops the ball entirely. Wage growth and margins are both high, following rounds of stimulus. A good economist would connect this to increasing spending and growth in the post-COVID era and declare it the effect of an imminent boom (or burst). Yet, the article still blames it on some nebulous war between labour and capital.

Lump of Wealth

The article also commits what I call the “lump of wealth” fallacy, the concept that all increases in the wealth of one party must result in a decrease of wealth for the other. If wages and prices are both rising, it is more likely the result of a growing economy with a structure that exhibits such a result, such that both labour and capital will become better off in the long run. In effect, the pie is growing, even as its division is changing, so everyone can be better off. If you look at the data, “lower” occupations especially are having real wages rise (opposite of the Great Inflation).

In addition, we must recognize that many workers are also capital-owners who have benefited from hot markets, or have stimulus checks saved (as mentioned). These are cushions that could keep workers better off.

The Japan Tautology

One last, relatively minor but still important, mistake the article makes is treating Japan as having a normal macroeconomy:

After correcting for pandemic-related distortions Japan’s pay growth appears to be slowing to below 1% a year, suggest data from Goldman Sachs, a bank.

Japan, as any economist knows, is a very weird case. Japan’s market structures, receding growth, and extremely low inflation expectations mean it should not be analyzed alongside other countries in these scenarios.